*Disclaimer: this blog was written long before I joined my current employer. It does not represent any of my current employer’s official thoughts whatsoever. Do not take anything in this article to be construed as financial advice in any way, shape, or form. This article simply contains personal musings that I wrote as a private citizen months ago.

Although 2020 has been a year to forget on most fronts, the torrid pace of technological innovation can be characterized a striking beacon of hope for humanity as we anticipate a return to our lives. However, when we consider 2020 milestones like the first mRNA vaccines, dazzling cost compression of Li-ion batteries, and the accelerating adoption of bitcoin, it is critical to note that few innovations randomly and unpredictably emerge like Heisenbergian protons. Behind every news headline lies years of dizzying, incremental progress that is largely abstracted from public view. It is only after a certain period of progress compounding that innovations creep into our lives in a significant, permanent way. When this happens, harkening back to picture life without said technology becomes almost impossible. For example, try to imagine a day without touching your iPhone. It’s inconceivable. However, we should recall that the first mass-market phones with touchscreens began to emerge years prior to the iPhone to much less fanfare (see the IBM Simon or Palm Pilot). Or let’s recall the absolute graveyard in consumer internet in the early 2000’s after the Dot Com bubble popped in 1999. You see, innovation seems to come at us suddenly, gradually, and then suddenly.

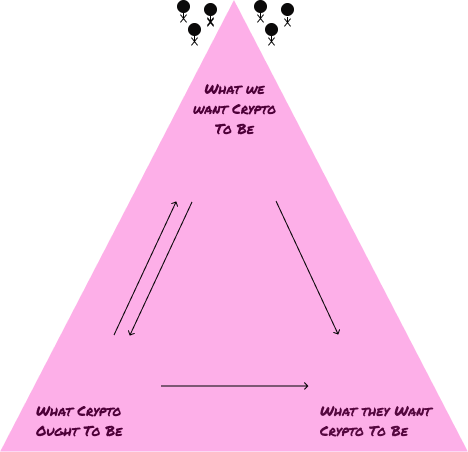

As 2021 is only days away, I’ve been reflecting specifically about what crypto trends and technologies might suddenly capture our attention in the upcoming year. For some reason I really enjoy thinking specifically about the future of crypto — perhaps it is the belief that no certain path has yet been bulldozed, and so crypto can very much become what we want it to be. The realization that each of us has the power to directly influence the future of a product or technology is an exciting, yet quite frankly, sobering realization that I learned early on at Square. And so, what do we want crypto to be? We are undeniably at a major inflection point in the eventual history of crypto whereby what we want crypto to be can very well either become what crypto ought to be or what they tell us crypto should be.

The phrase “what they want crypto to be” refers to the increasing regulatory scope of Western governments on crypto. Yes, few likely believe that the State should be completely laissez faire such that terrorist financing or large scale tax evasion/money laundering is permitted. However, what they tell us crypto should be is a dangerous solitary paradigm by which to construct the universe of crypto because it infringes upon the core tenet that open is better than closed source and because it leads to a world where innovation is stifled by undue regulatory capture rather than by market forces. If the West collectively moves forward with an innovation model for crypto where the primary market stakeholder becomes the State, the East will eat our lunch.

And so, what are some aspects of the crypto world we should look forward to in 2021 that take into account the ongoing battle between the dueling forces of what we want crypto to be, what crypto ought to be, and what they tell us crypto should be? Let me attempt to unpack a few here now.

A FEW Top of Minds for 2021

(not an exhaustive list to be clear)

Extension of Regulated Onramps from TradFi to DeFiThe continued collapse of investment-grade debt yields will likely continue into the early 2020s as central banks coordinate their continued and unprecedented monetary expansion that has exploded M1 supply to almost 7T USD in the US alone. This spike of +70% YoY in M1 supply has never before been seen in modern economic times (previous high since 1970’s is 20% YoY). The implications of this are obviously real, even if we cannot feel them today. A reckoning is coming and the almost 27% of global investment grade debt that is negative yielding will face the existential question whether to accept continued capital erosion when other alternatives exist. Additionally, there is something like $60T of global bank deposits that are currently low or zero yielding. What has the response been?

Well, we are starting to see legitimate TradFi (traditional finance) players take a nibble at crypto as the space has become increasingly legitimized with institutional-grade infrastructure (i.e. full-service prime brokerage, qualified custody, deep fixed/float borrow/lend markets, robust derivative offerings). But in many ways, institutional forays into crypto have started and stopped with bitcoin because of the lack of regulated onramps elsewhere, namely in DeFi (decentralized finance). In 2021 we will see these walls fall, and a rush of capital will enter DeFi as investors consider the value of unique DeFi products that enable novel consumer experiences and democratize access to basic financial services. In 2020 we saw the total value locked (TVL) in DeFi balloon from something like $1B to $15B — I think we will see an acceleration of TVL in 2021 to north of $100B.

Of course, with DeFi rails we can generate a more optimal risk-adjusted yield on basic financial products like savings deposits or receivables financing through automated yield aggregators and by cutting out legacy TradFi inefficiencies. It is not out of the normal to see high single digit APYs on rather common stablecoins — for instance, you can currently get paid nearly 12% APY to lend out your USDC, which is for all intents and purposes is a fully-collateralized, audited, risk-minimized dollar synthetic.

So, why have we not seen a popular consumer DeFi app take off yet? Where is the Revolut or Cash App of DeFi at? In my view, there are currently three main limiting factors: one, there are effectively zero DeFi projects which natively feature FDIC-style regulated deposit insurance against a hack or theft. Two, I don’t think entrepreneurs have been intentional enough in abstracting away the complexity of interfacing with crypto yet in their app UI/UX. I believe users will not realize they are interacting with DeFi rails when the first wildly successful DeFi application takes off. Lastly, the cost of cutting through the hoops of regulatory red tape is cost-prohibitive in terms of both time and dollars — elements that startups are perpetually short of. Tee it up to a systemic chicken and egg problem.

However, we have seen the tide turn in recent months as select teams have began to bear the brunt of regulatory compliance — for example, Aave recently obtained an EMI license in the EU which can be a roadmap to guide DeFi forward.

Crossover of Traditionally Insured Financial Products in DeFiThe other cool thing about Aave (as of v2) is how it natively embeds insurance-like properties into its platform, which should help to partially de-risk entrepreneurs building on top. But decentralized insurance in Aave and across DeFi more generally is in its early infancy, and is far removed from anything that represents the analog finance world’s investor protections. While I remain incredibly bullish on decentralized insurance systems (i.e. Nexus could be worth billions), if you want to compel Calpers to deploy $1T into DeFi tomorrow, you’ll be laughed out of the boardroom by telling their IC they are insured only by a decentralized mutual. There must a bridge from where we are today to the eventual decentralized state we hope to reach one day. I think this bridge must include DeFi products which are fully regulated by a jurisdiction and insured by traditional analog players like Lloyd’s of London.

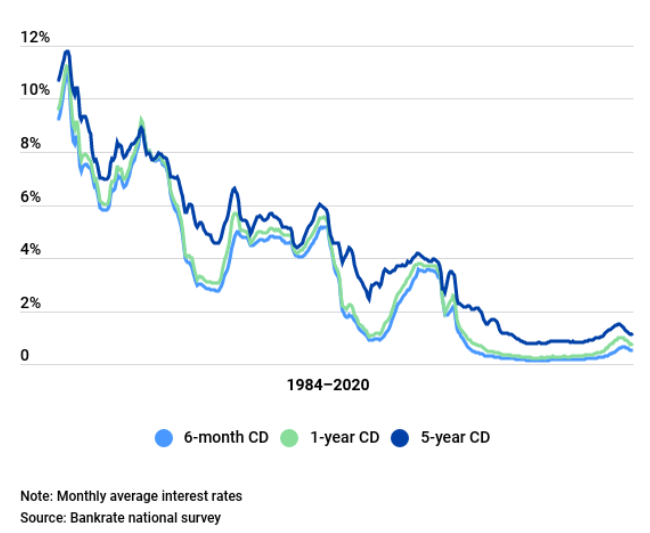

In 2021, I foresee we will see a rush of these new products that will attract tens of billions of USD deposits. In my view, the lowest hanging fruit here are insured savings accounts. As the chart below illustrates, DeFi savings accounts can massively outperform CD’s — historical CD interest rates have plunged over the past few decades from 10%+ to sub-1% today. According to the FDIC, the average yield on US savings accounts is just 0.06%. Even a best-in-class open banking application like Chime can only return 0.05% APY to savers.

https://www.bankrate.com/banking/cds/historical-cd-interest-rates/

Given how open banking is more conducive to crypto primitives because of the reliance on composable APIs for core application flows, I would think consumer-grade open banking applications should be scrambling to figure out how to pipe in DeFi rails to their products in a regulated and compliant fashion. However, until this happens (and it will happen slowly), I believe emerging DeFi-native banking applications will first experience rapid user growth. At this point, legacy neobanking franchises will have to choose whether to improve their offerings through defensive M&A or whether to replicate DeFi ramps in-house. I’m also thinking of a third option here that does not exist today, but very much should ;)

Crossover of fully homomorphic encryption into tokensWhen I worked with NuCypher my eyes were opened to the most wonderful world of fully homomorphic encryption, which in reality is a sort of voodoo magic that enables privacy-preserving computation on extremely large global datasets. Basically, FHE allows for search and compute on encrypted data. The implications are staggering — for example, without revealing one’s identity, every human could be compensated for streaming their genomic data to dynamic models constructing new drugs and cures for our most severe diseases like breast cancer. I’ve been on the search for companies attacking FHE, but the space has been somewhat slow to progress since…FHE is a really freaking hard problem to solve. NuCypher is still leading the charge here, and IBM and Inpher are also involved. It also appears that Algorand is involved given that one of the forefathers of FHE, Craig Gentry, is currently a researcher at the Algorand Foundation. I haven’t seen any public comment from Algorand on their FHE efforts though. In any event, I believe we’ll see a fully-functional FHE private smart contract design on testnet by the end of 2021.

Crossover of NFTs into Unique, Digitally Native ArtI can’t stop thinking about NFT digital art. I know, I know — NFT art can’t have value because it can “simply be screenshotted”. This sentiment is to be expected as moving from an analog model literally tens of thousands of years old to a fully digital one will require a massive tectonic shift in humans’ mental model for what is art.

However, in response I would instruct skeptics to check out Async.Art for a glimpse into how the digitally native canvas can provide uniquely experiential value. On Async.Art and other emerging competitors, digital artwork can be split into “layers” whereby the artist can attach an NFT to several components of the underlying artwork. What this means is that the totality of a piece’s token holders have the power to individually dictate how their respective layers appear and act on the digital canvas. For example, in the artwork below called ‘Akinya and June Wing’, one can purchase an NFT to represent the plane or an NFT for various colored shades of Akinya and June Wing. This leads to fully customizable and dynamic art, the state of which is trustlessly guaranteed via the blockchain. You can imagine how if a piece like this becomes quite valuable one day, having a claim to elements of it (i.e owning the plane) could also be quite lucrative.

Akinya and June Wing by Ytje Veenstra

I think the development of NFT-based art is underrated one of the most significant developments of human expression in history. Again, the ability to create fully customizable and dynamic pieces of art will flip the definition of art on its head. There are other aspects of NFT art that I also find compelling, like VR-native art (i.e. JOY will be seen as a Picasso-like figure in 50 years), as well as the ability to turn previously unproductive assets (i.e. art hanging on your wall) into instantly productive assets. For example, one can utilize emerging services like NFTfi to collateralize one’s NFTs to borrow/lend.

This is one of the oldest Joy’s. I love how trippy each Joy is. The artist seemingly intentionally has created a world where each piece takes on an identity that only the NFT owner chooses.

A Unipolar Liquidity Model Forks Bipolarly One of the more interesting developments of 2020 was when Uniswap was forked into SushiSwap. At first, Sushi was ridiculed as nothing more than a copycat. Even worse, the founder Chef Nomi did the unthinkable and rug pulled his community by selling his entire stash of ETH. This action crossed the line for me — a founder without any skin in the game is completely misaligned with their users. We’ve seen this story before when Charlie Lee famously sold all of his Litecoin worth hundreds of millions USD a few years ago, and LTC proceeded to plummet 90% from its high as active development on the coin basically grinded to a halt. In any event, Chef Nomi ended up returning all of the sold ETH to the Sushi treasury and asked the community to provide any sort of lockup schedule it deemed appropriate. At the time, I thought the initial selling event was unforgiveable and therefore proceeded not to pay much attention to SushiSwap. But in the past few months, SushiSwap has registered impressive user metrics which has caused me to reconsider my position that Uniswap had built an insurmountable competitive moat.

SushiSwap has gained a foothold as its TVL is now something like only 30% lower than Uniswap’s at $1.15B. In part due to the compressed cost of moving capital and in part due to growing product-market-fit, Sushi’s TVL has skyrocketed in the past month by over 4x. Pretty insane for a forked project. But it’s been quite a nice development to see an active, dedicated, and sticky community form around SushiSwap. They also ship new product like madmen.

It’s also interesting to consider how Sushi is attacking a slightly different customer segment than Uniswap. Uniswap has opted for a horizontal approach aiming to serve the long tail of assets with the deepest liquidity pools, but has a rather plain vanilla product. On the other hand, Sushi has taken a vertical approach, creating a deeper moat based on differentiated products (i.e. Onsens) and incentivized liquidity onramps from partners like Binance. The Binance partnership is quite intriguing as it signals an ongoing bifurcation of AMM liquidity provision between the East (Sushi) and the West (Uniswap). Although I remain bullish on Uniswap and others who have occupied similar AMM niches (i.e. 1inch for power traders), I think we’ll see Sushi dominate AMM usage in the East and Uniswap will dominate the West. With that said, it’s sort of crazy the Sushi is trading ~10x lower than Uniswap but only has like 30% lower TVL. Oh by the way, one can stake their Sushi tokens and generate upwards of 30% APY whereas as of v2 Uniswap my UNI tokens are totally unproductive without incurring the risk of impermanent loss.

Forks Are Perpetual A/B TestsWe’ve recently seen an explosion of stablecoins that are attempting to create a truly uncensorable, persistent, and decentralized stable money not pegged to any legacy fiat asset. I won’t comment on the merits of any particular one other than to say we’ve seen intriguing approaches thus far from players like ESD and Frax. Rather, what particularly interests me is the nature of how these experiments are being run. Because that’s effectively what these forks are, experiments.

It’s almost as if new experiments are being launched daily with a few select variables tinkered in order to reach a more optimal bootstrapping, liquidity provision, and stability mechanism. The cost to forking these experiments is zero and new projects are free to learn from prior projects’ mistakes. As I recently tweeted, the cynical view of these stablecoin forks is that they are simple copycats, but in reality they are one A/B test after another, with learnings from previous experiments embedded into what becomes an incrementally more optimal system design. Another profound realization for me is that we have effectively transformed our static, linear experimentation model for testing new products into a continuous, dynamic one. I think the implications of this are being played out in real time — namely, this should have a compounding effect on the speed of innovation.

My take on how dynamic experimentation is being utilized by new stablecoins

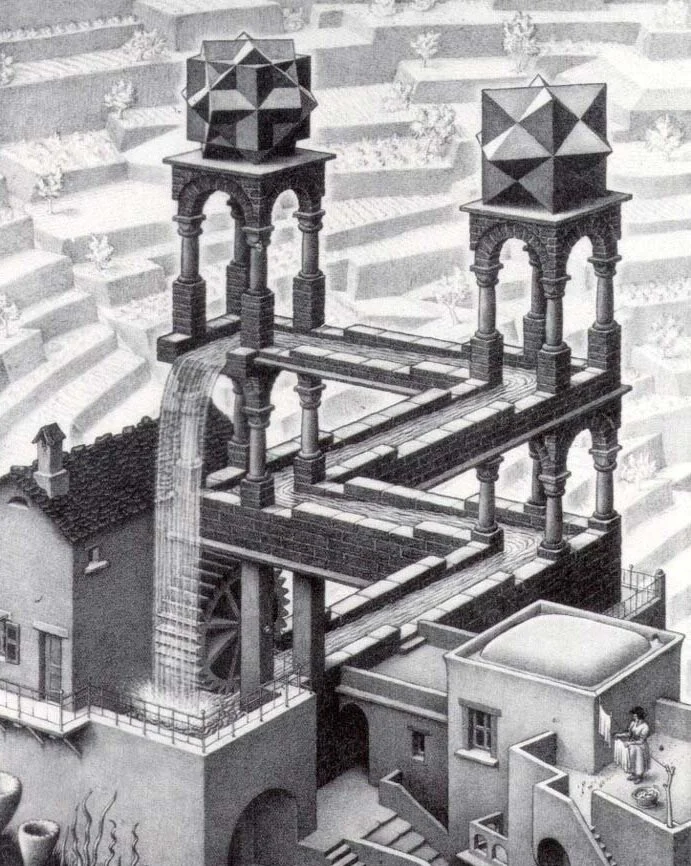

As communities coalesce on these various live experiments, old experiments can consume new learnings from new experiments and vice versa. In this case, we’ve effectively created an MC Escher-esque model of incrementing progress in the stablecoin space, that honestly will probably accelerate the discovery of an optimal solution by years.

One of my favorite MC Escher’s, “The Waterfall”, which details the old feeding the new and the new feeding the old.

Few Thoughts on the Intersection of TradFi x DeFi

In 2021, I think we’ll see an ETF and we’ll begin to see an explosion of regulated main street investment products like bitcoin IRAs (see AltoIRA). There will be a storm of M&A in 2021 as traditional financial institutions realize they are screwed if they continue to do nothing. Building technical and product expertise in-house is of course an expensive and time-intensive task that banks quite frankly may not be able to stand up to. It will be interesting to see what Coinbase does after it IPOs and amasses billions of dollars of a newfound war chest that they could use to aggressively acquire competitors rather than fund development in-house. If I were State Street, Fidelity, and some of the other global behemoth qualified custodians, I would be freaking out about getting cut out of a multitrillion dollar asset class without a beachhead comparative product for their institutional base. However it makes sense that institutional players, especially large scale ones like pensions and sovereigns will want a one-stop full-stack prime broker who can service both their equity, fixed income, and crypto assets. With that in mind, Coinbase should be worried that State Street will wake up a proud new owner of a player like Bitgo or NYDIG.

In closingTo sum it up, I’m so freaking excited for what crypto does in 2021. To be witnessing a truly fundamental transformation of our society for the better with crypto is truly amazing. While we may witness a serious amount of price and regulatory volatility, I do believe we will end 2021 with an aggregate crypto market cap north of $2.5T. With that, I want to give a big cheers to a great year ahead as crypto continues to move from suddenly and gradually, to suddenly.

*this is not financial advice